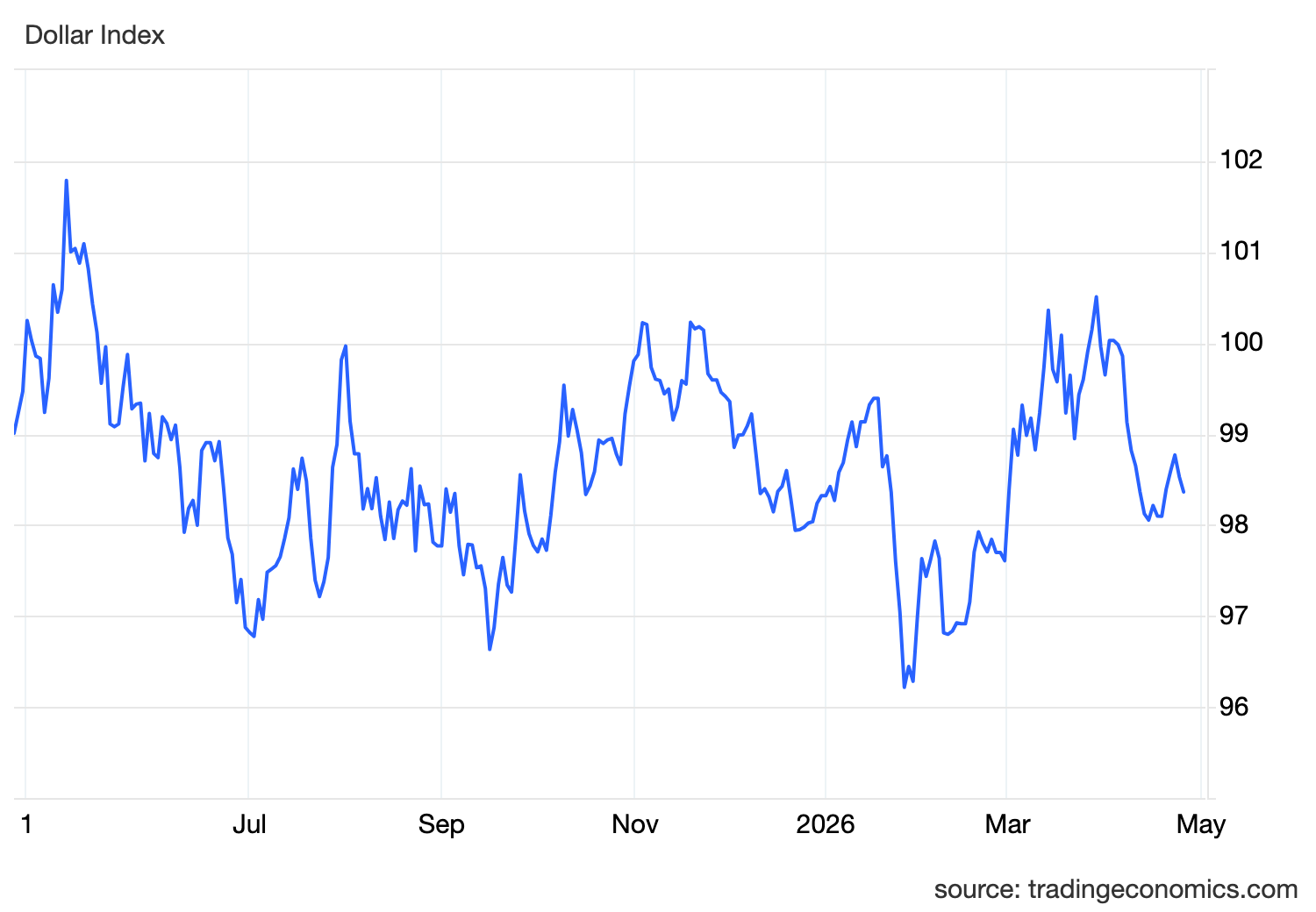

The dollar move here is about shifting expectations, not weakness.

After briefly pushing higher, the dollar reversed as markets reacted to signs of potential de-escalation between the US and Iran. A new proposal, delivered through Pakistani mediators, points toward a possible extension of the ceasefire and a path to reopening Hormuz.

That changes the tone.

Because once Hormuz is back in play, the oil risk premium starts to come out.

Earlier in the session, the opposite dynamic was in control. Comments from Donald Trump about canceling envoy-level talks pushed the dollar higher, as markets priced renewed tension and sustained supply disruption. But the later proposal from Iran forced a rethink.

This is the core driver.

Oil expectations.

When the market sees a credible path to easing supply constraints, oil comes under pressure. When oil softens, inflation expectations begin to ease. And when inflation expectations ease, the urgency for restrictive policy declines.

That is where the dollar loses momentum.

The Federal Reserve is still expected to hold rates steady at the upcoming meeting, likely one of the final meetings under Jerome Powell before a transition toward Kevin Warsh. But the key is not the decision itself. It is the forward guidance.

If inflation risks are seen as easing due to lower energy pressure, the Fed gains flexibility. It does not need to push back as hard on easing expectations. That softens yields, and by extension, softens the dollar.

At the same time, safe-haven demand is also fading slightly. Reduced geopolitical tension removes one of the pillars that had been supporting the currency.

So both drivers are shifting in the same direction.

Less inflation pressure. Less defensive demand.

That is why the dollar is pulling back.

Going forward, everything depends on whether this proposal leads to actual progress. If Hormuz reopens and oil declines, the macro setup shifts toward easing inflation and a more balanced policy outlook.

If talks break down again, the move reverses quickly.