The Fed is not moving, but the pressure is building.

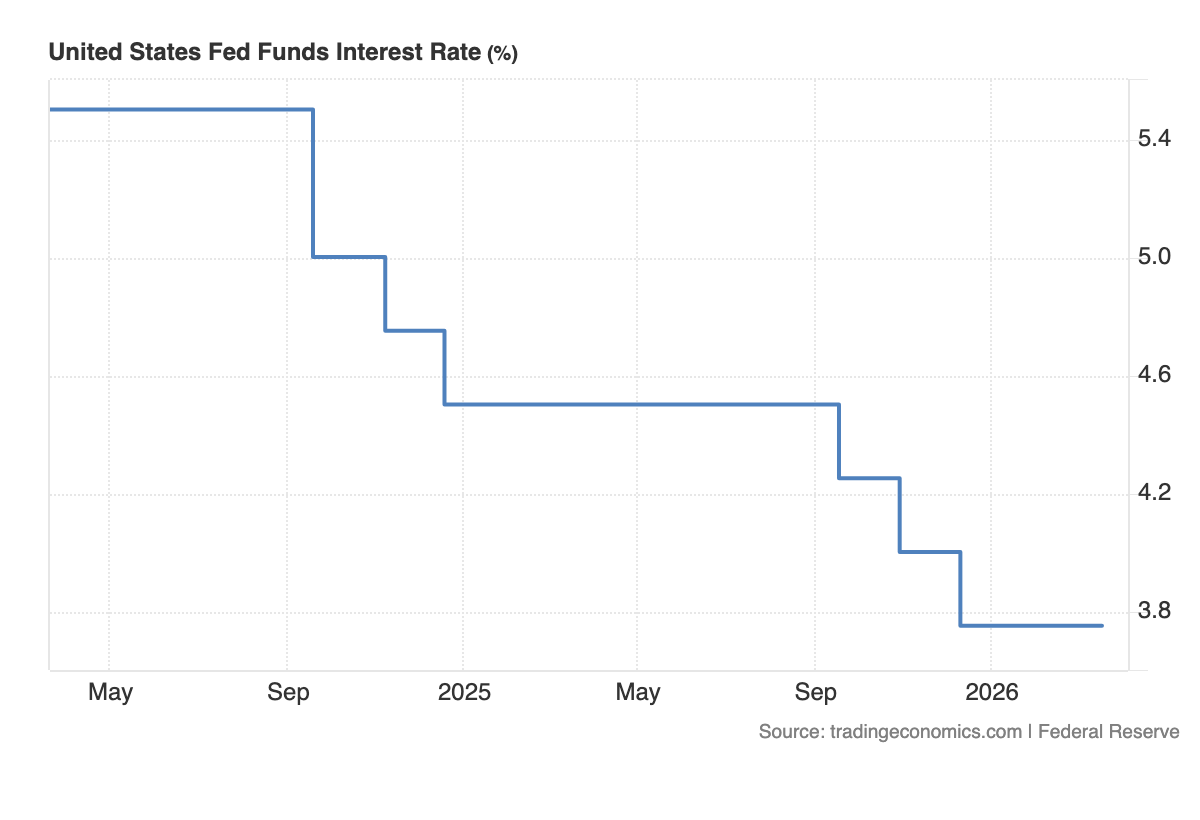

Markets expect rates to remain unchanged at 3.5% to 3.75%, marking a third consecutive hold. That decision is straightforward. The environment behind it is not.

The problem is oil.

Rising energy prices are feeding directly into inflation at a time when the economy is still holding up. The labour market remains resilient, and broader activity has not slowed enough to justify easing.

So the Fed is stuck.

Inflation is not fully under control, but growth is not weak enough to force a pivot. That leaves policymakers in a holding pattern, waiting for clearer signals.

This is where the reaction function becomes critical.

If oil continues to push inflation higher, the Fed cannot move toward rate cuts. Even if underlying inflation was easing before, energy shocks change the picture by keeping expectations elevated.

At the same time, the Fed is not eager to hike aggressively into a still-fragile global backdrop.

So policy stays restrictive, but cautious.

That is why markets are leaning toward no changes this year. But that view is not risk-free. If inflation accelerates further due to energy, the idea of additional tightening could come back into focus.

Leadership transition adds another layer.

This meeting may be the final one under Jerome Powell, with Kevin Warsh expected to take over in May. Warsh has already signaled a focus on maintaining independence and addressing persistent inflation, which suggests continuity in a cautious stance rather than a rapid shift.

For markets, the implications are clear.

Yields remain supported as policy stays tight. The dollar holds a firm base due to both rate differentials and uncertainty. Risk assets face a more challenging environment as liquidity expectations remain constrained.

Gold also struggles in this setup, as higher real yields increase the opportunity cost of holding non-yielding assets.

So the story is not about what the Fed is doing today.

It is about what it cannot do.

And right now, it cannot ease.

Filed under